Type

Trend follower

Short introduction

The Adaptive Moving Average was developed by Perry J. Kaufman. Kaufman assumes that in sideways market phases it is advisable to increase the length of the trends under consideration, for example the number of periods of a moving average indicating the trend direction, in order to reduce the number of trend changes displayed in such phases. The result of his deliberations is a trend instrument that adapts independently to the prevailing market situation. As a basis, he follows the variable moving averagescheme, whereby he defines a "noise" as a varying variable, a measure of the undirected mobility of prices or their reciprocal value, the so-called efficiency factor.

Formula/calculation

slow = 2 / (slow periods + 1)

fast = 2 / (fast periods + 1)

EFt =|Ct -Ct-n|/ (|Ct -Ct-1|+ (|Ct-1 -Ct-2|+ ... +|Ct-n+1 -Ct-n|)

wt = (EFt * (fast - slow) + slow)²

KAMAt=(1 -wt) *KAMAt-1 +wt * C

where:

w = adapted smoothing factor

EF = efficiency factor

fast periods = fastest trend in periods

slow periods = slowest trend in periods

n = number of periods for the consideration of movement efficiency

Statement/Interpretation

The following literature is recommended for the statement and interpretation of KAMA:

-

Kaufman, Perry J.: Trading Systems and Methods, Wiley, 1998

-

Kaufman, Perry J.: Smarter Trading, McGraw-Hill, 1995

-

Florek, Erich: New Trading Dimensions, FinanzBuch Verlag, 2000

-

Müller, Thomas and Lindner, Wolfgang: The big book of technical indicators, TM Börsenverlag

Default setting

-

n = 10

-

Fast periods = 2

-

Slow periods = 30

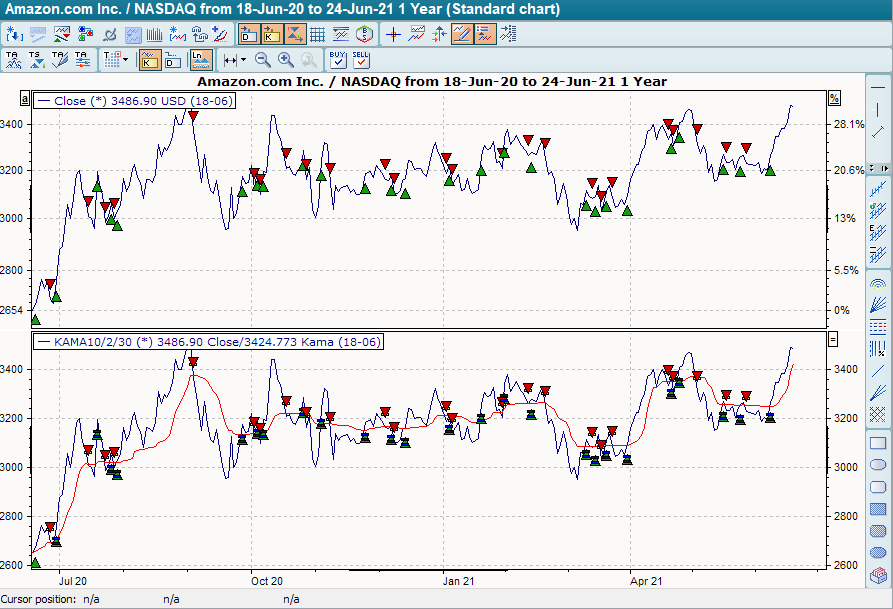

Basic trading systems

-

KAMA

In the basic trading system "KAMA", the default setting of the parameters is: for the period 10, the fast period 2 and the slow period 30. The base trading system provides buy signals when the close breaks through the indicator from bottom to top and sell signals when it breaks through the indicator from top to bottom.