Module "Portfolio Service Extended Portfolio Analysis"

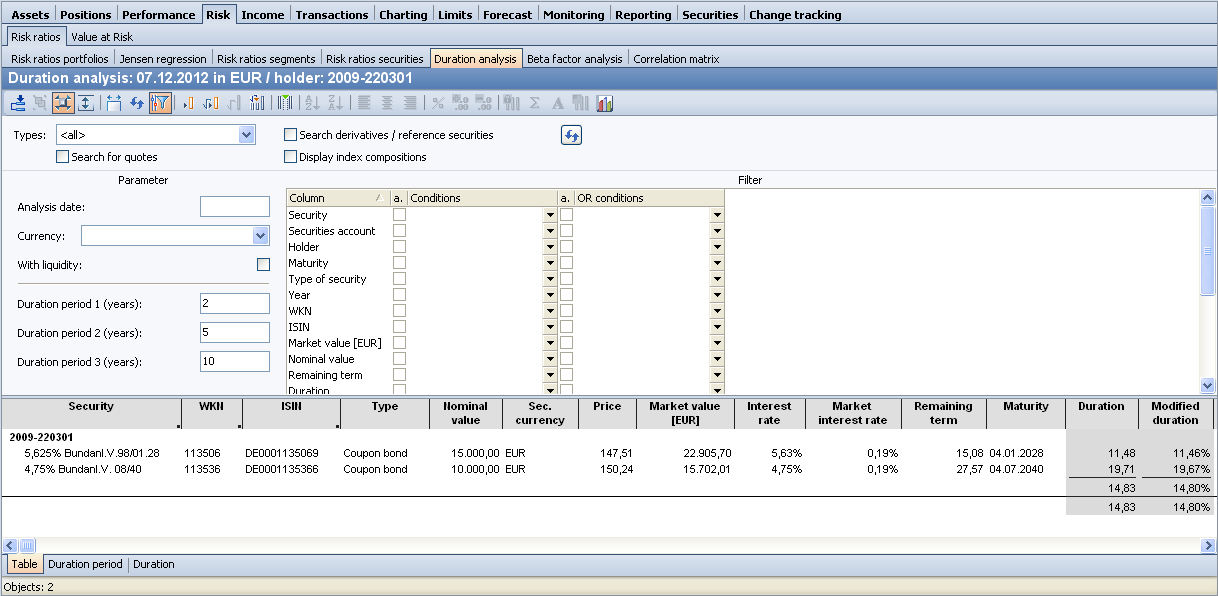

You can find the duration analysis in the workspace of holders, portfolios or groups on the worksheet "Risk", "Duration analysis".

The duration analysis relates exclusively to the bond positions and fixed-term deposits in a portfolio. The following are included in the analysis:

-

Bonds of the "coupon bond" type

-

Zero bond" type bonds

-

Floater

-

Pension funds

-

ETF bond funds

-

Fixed-term deposit

The duration of bond funds is not calculated by the program. Rather, it is delivered as a master date as part of the"Fonds Plus" subscription.

The duration analysis shows the key figures duration, modified duration and convexity for each bond and for fixed-term deposits.

The details of the most important columns and rows of the evaluation can be found in the following table:

|

Column |

Description |

|---|---|

|

Type |

Zero bonds, coupon bonds, (bond) funds or floaters and fixed-term deposits. |

|

Interest rate |

Interest rate of the position in percent. |

|

Market interest rate |

Available market interest rate in percent. |

|

Remaining term |

Remaining term of the item in years in relation to the "Evaluation date" parameter. |

|

Duration |

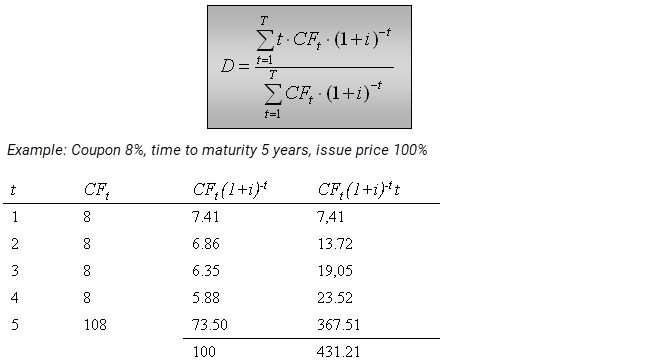

Duration is a key figure for assessing the risk of bonds. It is to be understood as the average commitment period of the capital employed in years. For details, see the following example and refer to the relevant literature, e.g. Steiner, Manfred, Bruns, Christoph and Stöckl, Stefan: Securities Management; 10th edition; from p. 168. In this context, please also note the information in the section Literature. |

|

Modified duration |

The modified duration is calculated from the duration and is a measure of the actual interest rate sensitivity of the bond. |

|

Convexity |

In contrast to duration, this key figure takes into account the convex shape of the bond price trend depending on changes in market interest rates. Here too, please refer to the further literature for precise calculations. |

|

Yield |

Bond yield (on basis 1). |

|

Duration period |

You define the limits of the intervals in this column using the parameters Duration period 1 to 3. See the following chapter Parameters of the duration analysis. |

D= 431.21100=4.31 years

Dmod = 11+i ×D =3.99 %

where:

CF = Cash flow

t = period

i = interest rate

D = Duration

Dmod = Modified Duration