Module "Portfolio Service Extended Portfolio Analysis"

Standard restriction schemes are already included in the delivery state, which you can use to configure a large number of conceivable restrictions without any problems - without having to open the formula editor for the MM-Talk definitions.

These supplied standard restriction schemes are briefly presented in this section. You can use the simple examples to configure individual restrictions for monitoring your portfolios. However, you can also create completely new restriction schemes using the MM-Talk formula language.

Restriction scheme "No ⟨WP⟩"

Use this restriction scheme as the basis for portfolio restrictionsthat monitor that certain securities are not in the portfolio's securities accounts. Use the "WP" parameter to select the security to be excluded when creating the restriction.

You do not wish to hold any Borussia Dortmund shares in your securities account. You want to monitor this specification with a stock restriction. Proceed as follows:

-

Select the RESTRICTIONS command on the "Configuration" tab.

The "Configure restrictions" dialog box appears by default with the "Restrictions" tab open. -

-

Now select the "No <WP>" schema in the "Restriction schema" selection list on the right-hand side.

-

Select the "Parameters" button.

-

Select the "Search" icon of the "WP" parameter and search for the security to be monitored. Select the security ("Borussia Dortmund" WKN "549309") in the search result.

Unknown Attachment -

Confirm the entry of the parameter value with "OK".

-

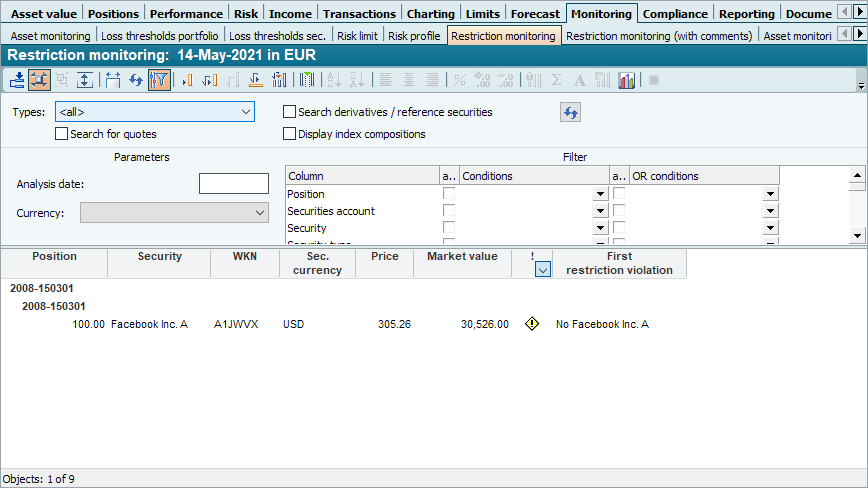

The newly created restriction is automatically given the name "No Borussia Dortmund".

-

Confirm the "Configure restrictions" dialog box with the "Save" button.

The "No Borussia Dortmund" restriction is now available and can be assigned to a portfolio, for example, as described in the section Assign restrictions . For portfolios containing this share, this restriction then results in a restriction violation in the "Restriction monitoring" evaluation.

Restriction scheme "No ⟨master date⟩ ⟨expression⟩"

Use this restriction scheme as the basis for position restrictionsthat monitor that securities with certain master data are not in the portfolio's securities accounts. When creating the restriction, use the "Master data" parameter to select the data field (e.g. "Country") and the second parameter "Characteristic" to specify the value to be excluded (e.g. "Austria").

There is a choice:

-

Issuer

-

Country

-

Industry

You can edit this restriction scheme at any time using MM-Talk, e.g. to include additional master data.

Please also read the section Create restriction schemes.

Restriction scheme "No ⟨classification⟩ ⟨class⟩"

Use this restriction scheme as the basis for portfolio restrictionsthat monitor that securities from certain asset classes are not held in the portfolio. When creating the restriction, use the "Classification" parameter to select the asset classification (e.g. "Asset class") and the second "Class" parameter to specify the value to be excluded (e.g. "Equities").

All configured asset classifications are available for selection here, e.g:

-

Asset class

-

Region

-

Segment

-

Currency

-

Risk classification

-

..

You can find out how to create asset classifications in the chapter Edit basic asset classes and asset classifications.

Restriction scheme "⟨WP⟩ max. ⟨percent⟩"

Use this restriction scheme as the basis for quota restrictions, which monitor that the proportion of a security in the portfolio does not rise above a certain limit. When creating the restriction, use the "WP" parameter to select the security to be monitored and the second parameter "Percent" to specify the upper limit for the share of the portfolio by entering a number (e.g. "5" for "5%").

When entering percentage values, for example, both "5" and "5%" are permitted. The percentage sign is displayed correctly both in the name of the restriction and the next time the parameters are opened.

Restriction scheme "⟨Classification⟩ ⟨Class⟩ max. ⟨Percent⟩"

Use this restriction scheme as the basis for quota restrictions, which monitor that the share of a certain class of an asset classification in the portfolio does not rise above a certain limit. When creating the restriction, use the "Classification" and "Class" parameters to select the asset class to be monitored, and use the third parameter "Percent" to specify the upper limit for the share of the class in the portfolio by entering a number (e.g. "25" for "25%").

As with the corresponding stock restrictions, all configured asset classifications are available for selection here, e.g:

-

Asset class

-

Region

-

Segment

-

Currency

-

Risk classification

-

..

You can find out how to create asset classifications in the chapter Edit basic asset classes and asset classifications.

Restriction scheme "⟨Date of origin⟩ ⟨Expression⟩ max. ⟨Percent⟩"

Use this restriction scheme as the basis for quota restrictionsthat monitor that the share of a certain issuer, country or sector in the portfolio does not exceed a certain limit. When creating the restriction, use the "Master date" and "Characteristic" parameters to select the value to be monitored, and use the third parameter "Percentage" to enter a number to define the upper limit for the proportion of the value in the portfolio (e.g. "25" for "25%").

The following data is available for selection here:

-

Issuers

-

Countries

-

Industries

You wish to invest a maximum of 25% of your portfolio in securities from Switzerland. You want to monitor this requirement with a quota restriction. Proceed as follows:

-

Select the RESTRICTIONS command on the "Configuration" tab. The "Configure restrictions" dialog box appears by default with the "Restrictions" tab open.

-

-

In the "Restriction scheme" selection list in the right-hand area, select the scheme "<main date> <expression> max. <percentage>".

-

Select the "Parameters" button.

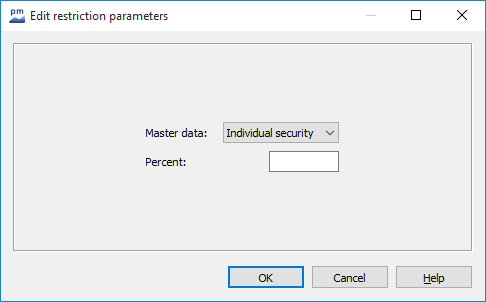

Unknown Attachment -

In the "Edit restriction parameters" dialog box that appears, select the "Country" entry in the "Master data" selection list.

-

Enter the value "Switzerland" in the input field for the "Characteristic" parameter.

-

Enter the value "25" in the input field for the "Percent" parameter.

-

Confirm the parameter value entries with "OK".

-

The newly created restriction is automatically given the name "Country Switzerland max. 25.00%".

-

Confirm the "Configure restrictions" dialog box with the "Save" button.

The restriction "Country Switzerland max. 25.00%" is now available and can be assigned to your portfolio as described in the section Assign restrictions . For portfolios that invest more than 25% of the portfolio value in securities from Switzerland, this restriction then results in a restriction violation for the corresponding securities in the "Restriction monitoring" evaluation.

Restriction scheme "Any ⟨master date⟩ max. ⟨percent⟩"

Use this restriction scheme as the basis for quota restrictionsthat monitor that the share of a master data does not rise above a certain limit. When creating the restriction, use the "Master date" parameter to select the area to be monitored and the "Percent" parameter to enter a number to define the upper limit for the respective shares in the portfolio (e.g. "25" for "25%").

The following dates are available for selection:

-

Single title

-

Issuer

-

Country

-

Industry

You want to invest a maximum of 10% of your portfolio in individual securities. You want to monitor this requirement with a quota restriction. Proceed as follows:

-

Select the RESTRICTIONS command on the "Configuration" tab. The "Configure restrictions" dialog box appears by default with the "Restrictions" tab open.

-

-

Now select the "Any <master date> max. <percent>" schema in the "Restriction schema" selection list on the right-hand side.

-

Select the "Parameters" button.

-

In the "Edit restriction parameters" dialog box that appears, select the "Single title" entry in the "Master date" selection list.

-

Enter the value "10" in the input field for the "Percent" parameter.

-

Confirm the parameter value entries with "OK".

-

The newly created restriction is automatically given the name "Any single security(s) max. 10%".

-

Confirm the "Configure restrictions" dialog box with the "Save" button.

The restriction "Any single security(s) max. 10.00%" is now available and can be assigned to your portfolio as described in the section Assign restrictions . For securities positions that account for more than 10% of the portfolio value, this restriction then results in a restriction violation in the "Restriction monitoring" evaluation.

Restriction scheme "⟨classification_1⟩ ⟨class_1⟩ max. ⟨percent_1⟩ or ⟨classification_2⟩ ⟨class_2⟩ max. ⟨percent_2⟩"

Use this restriction scheme as a basis for quota restrictionsthat check whether the market value shares of two classes from different classifications contain too many market value shares. The restriction is only violated if both conditions are not met.

This restriction checks whether a maximum of 50% is invested in equities or a maximum of 10% in the sub-asset class "Japanese equities". If both proportion limits are not observed, the restriction is violated.

Restriction scheme "⟨classification⟩ ⟨class_1⟩ + ⟨class_2⟩ max. ⟨percent⟩"

Use this restriction scheme as a basis for quota restrictionsthat check whether the sum of two different classes of the same classification contains too many market value shares.

This restriction checks whether the combined shares and bonds account for a maximum of 70% of the total portfolio.

Restriction scheme "No short selling"

Use this restriction scheme as the basis for quota restrictionsthat check whether the holding of a security is < 0. In this case, a short sale has taken place and the restriction monitoring reports a restriction violation.

This restriction does not require any parameters.

Restriction scheme "Foreign currency max. ⟨percent⟩"

Use this restriction scheme as the basis for quota restrictionsthat check whether the foreign currency quota is adhered to in accordance with the currency class classification. All positions in a currency other than the evaluation currency of the portfolio are regarded as foreign currency positions. The share is calculated on the total portfolio. Any liquidity in foreign currency is not taken into account.

This restriction scheme requires that the portfolio currency is entered in the "Currency class" asset classification under a corresponding abbreviation (e.g. "EUR").

This restriction checks whether at least 60% of the total portfolio is always invested in positions in the portfolio currency. If the proportion of foreign currency positions exceeds 40%, the restriction is violated.

Restriction scheme "Non-investment grade bonds max. ⟨percent⟩"

Use this restriction scheme as the basis for quota restrictionsthat check whether the proportion of bonds classified as "non-investment grade" on the basis of total assets is too high. Fitch, Moody's and Standard & Poor's ratings are reviewed. As soon as one of the rating agencies classifies the bond as "non-investment grade", the bond is considered as such.

Non-existent ratings ('n/a') are ignored and do not generate a breach, while unrated bonds ('nr') count as "non-investment grade".

The restriction violation is only displayed in the restriction monitoring for "non-investment grade" bonds.

If the "User-defined rating" master data field is filled, this always has priority and is considered exclusively.

This restriction checks whether a maximum of 10% of the portfolio's total assets are invested in "non-investment grade bonds" (share of the market value of the bonds concerned).

Restriction scheme "Investment grade min. ⟨percent⟩"

Use this restriction scheme as a basis for quota restrictionsthat check whether the proportion of bonds classified as "investment grade" is sufficient on the basis of total assets. Fitch, Moody's and Standard & Poor's ratings are reviewed. As soon as one of the ratings classifies the bond as "non-investment grade", the bond is considered as such.

Non-existent ratings ("n/a") are not taken into account in this review, while unrated bonds ("nr") count as "non-investment grade". This means that a bond is only "investment grade" if all existing ratings classify it as "investment grade". The restriction is deemed to have been violated if there are not enough investment grade bonds.

If there are no bonds in the portfolio, the restriction violation is indicated for all positions in the restriction monitoring. If there are bonds in the portfolio, the violation is displayed in the restriction monitoring for all bonds in the portfolio.

If the "User-defined rating" master data field is filled, this always has priority and is considered exclusively.

This restriction checks whether at least 30% of the portfolio's total assets are invested in "investment grade bonds" (market value share of the bonds concerned).

Restriction scheme "Cluster risk ⟨diversification⟩ max. ⟨percent⟩"

Use this restriction scheme as a basis for quota restrictionsthat check the cluster risk with regard to issuers, regions or currencies.

This restriction checks the cluster risk with regard to issuers: A maximum of 10% of the portfolio may be invested in one issuer.

Restriction scheme ⟨ESG category⟩ Score between ⟨minimum⟩ and ⟨maximum⟩

Use this restriction scheme as a basis for portfolio restrictions for your ESG requirements for your securities.

Parameters of the restriction scheme:

|

Parameters |

Default setting |

|---|---|

|

Minimum |

0 |

|

Maximum |

100 |

|

ESG category |

S4 (Community & Society) |

These portfolio restrictions are violated if the ESG score of an ESG category is outside the defined interval. By default, a breach is also reported for positions without an ESG score.

Restriction scheme ⟨ESG category⟩ score between ⟨minimum score⟩ and ⟨maximum score⟩, share of portfolio between ⟨minimum share⟩ and ⟨maximum share⟩

Use this restriction scheme as the basis for quota restrictions for your ESG requirements for your securities and portfolios.

Parameters of the restriction scheme:

|

Parameters |

Default setting |

|---|---|

|

Minimum score

|

0 |

|

Maximum score

|

100 |

|

Minimum share |

0 |

|

Maximum share |

100 |

|

ESG category |

S4 (Community & Society) |

These quota restrictions are violated if the share in the portfolio of securities whose ESG score for the corresponding ESG category is outside the set interval is outside the defined share interval for the portfolio.