Portfolio Risk Service" module

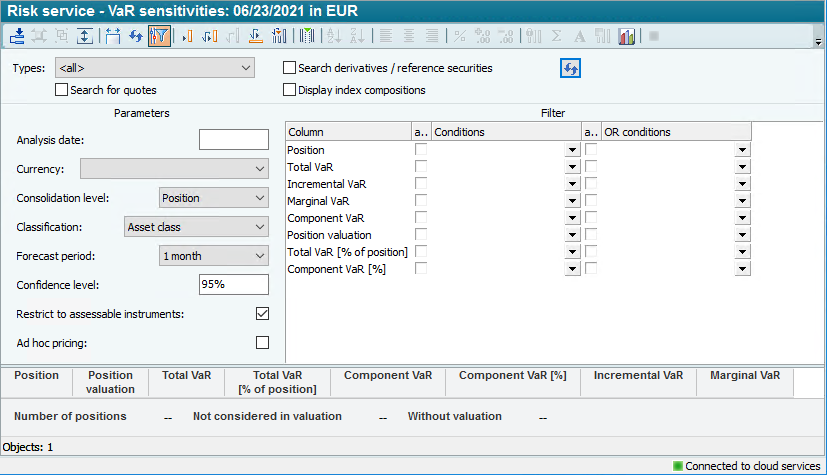

This evaluation represents a variant of the VaR sensitivities optimized for the risk service.

In the footer of the table you will find summarized information on the assessability of the items, which facilitates error analysis.

For details on the key figures, please read the VaR sensitivitiessection.