Bond scenario analysis" module

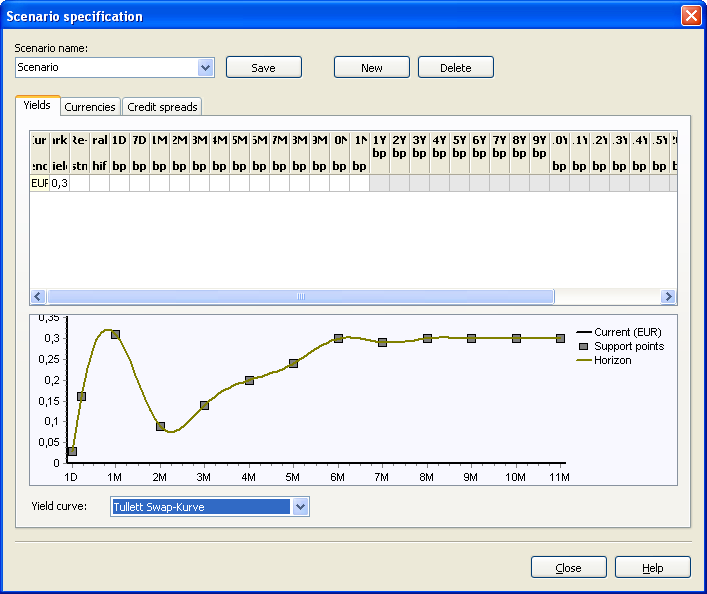

On the "Yields" tab, the parameters of the yield scenario form a table of (mainly maturity-dependent) shift values for each currency. The table contains the following columns:

|

Column |

Description |

|---|---|

|

Currency |

This column shows all currencies that belong to the current portfolio. |

|

Market interest rate 1Y [%] |

This column contains the 1-year value of the current yield curve as information for comparison with the next column "Reinvestment interest". |

|

Reinvestment interest |

In this column, enter the reinvestment interest rate for each currency for the simulation of reinvestment for repayments or interest payments. |

|

Parallel displacement |

In this column, enter the number of base points by which the horizon curve should be shifted. Note that parallel displacement and runtime-dependent displacements add up in the effect. |

|

6M [bp] ... 50J [bp] |

Enter the (residual) term-dependent interest rate differences for terms of 1 year to 50 years in basis points. |

The diagram below shows the current (settlement date) and the resulting horizon curve. Read the corresponding remaining terms on the x-axis and the yields on the y-axis. Changes in the table are immediately taken into account in the diagram.

In addition to entering maturity-dependent interest rate differences in the corresponding table cells, you can also change them directly in the diagram by dragging the grid points with the mouse.

ⓘ