Module "Portfolio Service Extended Portfolio Analysis"

The performance breakdown provides you with an analysis that helps you to understand the DVK (average available capital) and the performance or to check the values.

The performance breakdown is not anchored in the workspaces by default; you can find it in the list of templates in the "Depot management" category.

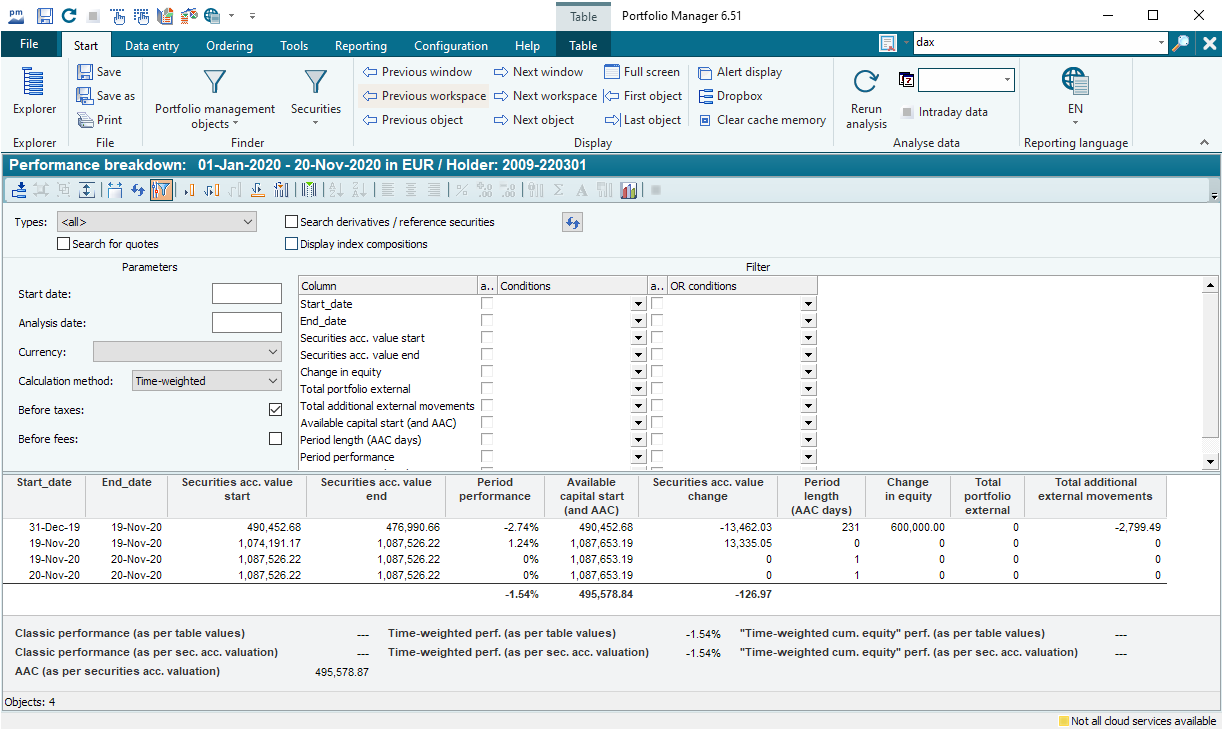

The columns of the "Performance breakdown" evaluation:

|

Column |

Description |

|---|---|

|

Start date |

The start date of the performance calculation. The calculation is made from the price on this day. You can set the start date using the parameter of the same name in the table. |

|

End date |

The end date of the performance calculation. The evaluation takes place at the end of the day. You can set the evaluation date via the parameter of the same name in the table or via the input field on the "Start" tab. |

|

Deposit value start |

The securities account value on the start date. In the case of time-weighted performance, this value is analogous to the function Depotbewertung.Depotwert at the start of the period (except for the second period in the case of two phases on one valuation day). In the "time-weighted cum equity" method, it also includes the equity difference and other exogenous cash flows for this period. |

|

Deposit value end |

The securities account value on the evaluation date. In the case of "Time value cum equity", this value is analogous to the function Depotbewertung.Depotwert. The time-weighted performance (in the case of "Method 1" in the section Calculation methods) does not include exogenous cash flows. |

|

Period performance |

The period performance according to the set calculation method in percent. |

|

Available capital Start (and DVK) |

Available capital at the beginning of the period, i.e. the securities account value at the beginning of the evaluation plus exogenous cash flows up to the beginning of this period. At the bottom of this column you will find the average available capital - calculated as a weighted average (available capital weighted by the respective period length). |

|

Change in securities account value |

The change in the securities account value results from the difference between the columns "Securities account value end" and "Securities account value start". |

|

Period length

|

The length of this period (in days) as used to calculate the DVK. This value depends on the setting "Calculate average available capital on trading days" on the "Securities account" tab in the global settings. |

|

EK change |

The value of incoming and outgoing deliveries as well as cash deposits and withdrawals in the period. |

|

Total portfolio-exogenous |

Sum of the portfolio-exogenous movements in this period from the perspective of the accounts. |

|

Sum of additional exogenous movements |

Depending on the configuration of the components to be regarded as exogenous (see section Configuring performance components), taxes and/or fees can be regarded as exogenous cash flows. The function returns the sum of these cash flows in the period. |

|

Values in the footer of the table |

|

|

Performance

|

The percentage performance determined on the basis of the values in this breakdown according to the calculation type currently set via the parameters. |

|

Performance

|

The percentage performance according to the portfolio valuation for comparison. |

|

DVK

|

The average available capital according to the portfolio valuation |

MM-Talk functions are provided for these columns, which provide the essential information required to calculate performance for each period of constant equity. You can find these MM-Talk functions in the section Functions on PerformanceCalculationInfo.

-

Depending on the configuration, taxes and/or fees are included in the DVK (more precisely: in the available capital for each period) and the time-weighted performance (calculated portfolio value at the end of the period).

-

The actual position value used is not always immediately apparent (order price substitution, interim profits).

-

The period length depends on the day calculation set in the options (stock exchange or calendar days).

-

Depending on the number of transactions in a day, the 2-period case may be time-consuming to track.

-

If there are no exogenous movements between the start and end dates, the table is "empty".

-

When calculating the time-weighted performance, the value of the securities account (object) is determined at the end of each day. The period limits (columns "Start date", "End date") are therefore to be interpreted as end-of-day times in this case. The exogenous movements (columns "Equity change", "Total portfolio exogenous", "Total additional exogenous movements") take place at the end of each period.

-

"Depot value end" refers to the value before the exogenous movements take place.

-

When calculating the DVK, it is assumed that exogenous capital flows take place at the beginning of the day. Therefore, the value in the "Period length (DVK days)" column in the first period is one day shorter than the calculated difference between the "End date" and "Start date" (as the calculation starts from the "Start date" parameter, but the "Start date" column contains a day earlier), and one day longer for the last period (as the "End date" day is calculated as a full day). However, if an exogenous movement takes place on the evaluation date, instead of extending the existing period, this generates a further period with the "period length (PL)" of one day, for which the corresponding new value for the capital available on this day is shown. This period has no influence on the calculation of the time-weighted performance, as the "Start securities account value" and "End securities account value" are identical.