The "Suitability report" evaluation checks the portfolio for suitability with regard to the investment profile stored. The "suitability report" is based on WM data, the risk calculation on the value at risk.

In the default setting, only the negative target market is compared with the investment profile in the "Suitability report". You can control this behavior using the "Negative target market" parameter, which is activated by default: Deactivate the parameter to obtain a complete target market profiling with positive and negative target market.

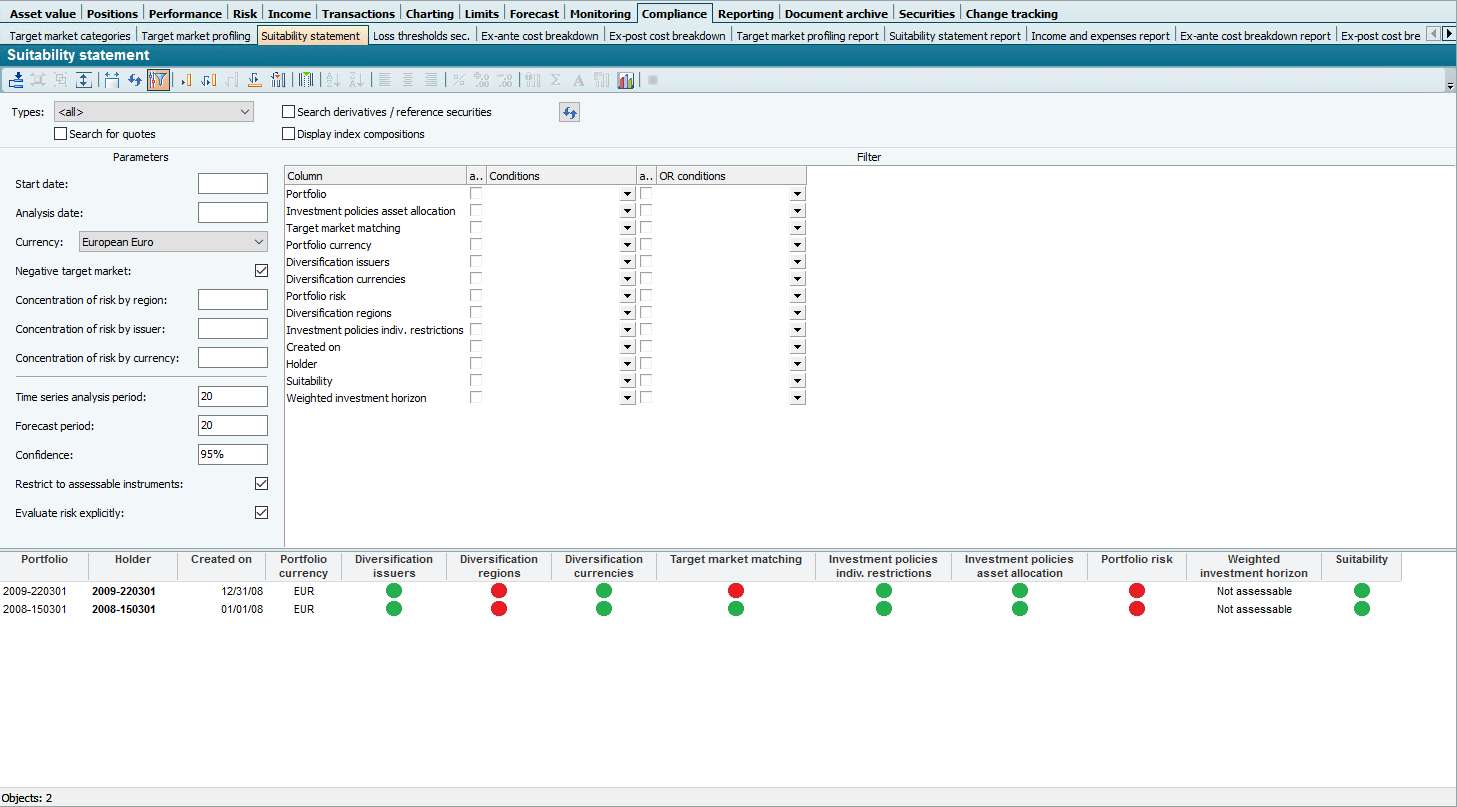

You can find the "Suitability report" in the "Compliance" worksheet in the Portfolios workspace, for example.

In detail, the "Suitability report" table contains the following columns:

|

Column |

Description |

|---|---|

|

Portfolio |

The name of the portfolio from the portfolio properties. |

|

Holder |

The name of the holder of the portfolio from the holder properties. |

|

Created on |

The "Created on" date from the portfolio properties. |

|

Portfolio currency |

The evaluation currency of the portfolio from the portfolio properties. |

|

Suitability check

|

|

|

Diversification Issuers |

The result of the review with regard to the diversification criterion "issuers" (of bonds). The colors of the symbols symbolize the result of the respective test:

If a check cannot be carried out, the results column remains empty. |

|

Diversification Regions |

The result of the review with regard to the diversification criterion "regions" (based on the asset classifications). |

|

Currency diversification |

The result of the review of the "currencies" diversification criterion (based on the asset classifications). If all currencies correspond to the portfolio currency, the "Currency cluster risk" is 0, i.e. this column is displayed in green. |

|

Target market comparison |

The result of the target market comparison. The new parameter "Negative target market", which is activated by default, is used to match the investment profile only with regard to the negative target market. Deactivate the parameter to also take the positive target market into account. |

|

Investment guidelines Individual restrictions |

The result of the check regarding the stored restrictions. |

|

Investment guidelines Asset allocation |

The result of the review of the deposited asset allocation. |

|

Portfolio risk |

The result of the portfolio risk review. Compliance with the permitted portfolio risk (value at risk) is checked using the SRRI risk intervals of the "risk/return" criterion. If you deactivate the "Explicitly assess risk" parameter, the portfolio risk is only checked with regard to its upper limit.

|

|

Weighted investment horizon |

The result of the review of the weighted investment horizon. The positions are weighted according to their share of the portfolio. In the preformula of the table, the intervals are divided into "short-term" (default setting up to 2.75 years), "medium-term" (2.75 to 5.25 years) and "long-term" (longer than 5.25 years). Please note that these values are not strict regulatory requirements, but merely useful examples. If necessary, adapt your suitability report to your individual values.

|

|

Appropriateness |

The result of the appropriateness review. |

You can hide columns that are not required in order to customize the analysis to your needs.

Use Report Suitability report, which is also included in the standard templates, to inform your customers about the results of the suitability tests.

You can find details on the special features for FinSA clients in the section Information on FIDLEG .