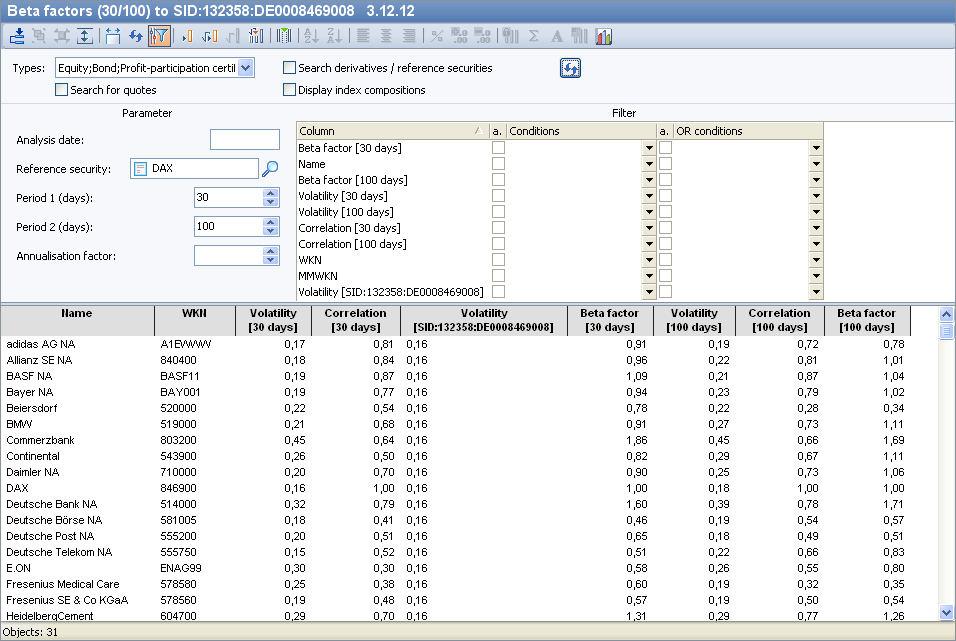

The "Beta factors" analysis provides an overview of volatility, correlation and beta factors.

The "Beta factors" evaluation is not in the workspace of a folder, filter or base value by default. Use the command OPEN WITH TEMPLATE... in the context menu of the Explorer objects or the <F10> key to open the evaluation in the "Open template" dialog box in the "Securities analysis" category.

You can find out how to set up your individual workspaces in the section Configure workspaces.

The details of the individual columns:

|

Column |

Description |

|---|---|

|

Name |

The name of the security (option, warrant, share...). |

|

WKN |

The security identification number of the security. |

|

Volatility [comparative value] |

The volatility of the benchmark in the first period indicated. |

|

Volatility Period 1 |

The volatility over the first specified period. |

|

Correlation Period 1 |

The correlation with the selected comparison value over the first specified period. |

|

Beta factor Period 1 |

Beta factor compared to the selected benchmark over the first specified period. |

|

Volatility Period 2 |

The volatility over the second specified period. |

|

Correlation Period 2 |

The correlation with the selected comparison value over the second specified period. |

|

Beta factor Period 2 |

Beta factor compared to the selected benchmark over the second specified period. |

|

Security no. |

The security number of the security. |

|

MMWKN |

The MMWKN of the security. |

Details on special parameters of the beta factors:

|

Parameters |

Description |

|---|---|

|

Settlement paper |

A comparative value must always be specified for the calculation of the correlation and the beta factor. In most cases, this will be an index. Enter the name of the desired comparison value here. As with all names, you only need to enter part of the name. Then start the search by clicking on the "Search" icon. |

|

Period 1 (days) |

First period for which the volatility, correlation and beta factor are to be calculated. The period usually comprises 30, 100 or 250 days. Other time periods are possible, but rather unusual. The default setting is 30 days. |

|

Period 2 (days) |

You can also specify an alternative calculation period for the volatility, correlation and beta factor here. The default setting is 100 days. |

If you do not make any changes/entries, the default settings are automatically used.

Read about the other parameters of the "Beta factors" evaluation in the section Parameters of the quantitative analysis evaluations.

Volatility

Volatility is a statistical value for the extent of the expected price movement and is expressed as a percentage. If a security has a volatility of 25%, a range of 25% upwards and downwards is to be expected within the next twelve months. This value is calculated on the basis of previous price movements over a specified period. The period usually comprises 30, 100 or 250 days. Other periods are of course also possible, but unusual.

Like all statistical methods, volatility is only an indication. No security will rise by 25% just because this was calculated using a measurement method. Price movements are still determined by supply and demand. The results from the quantitative analysis are merely an aid for comparing similar securities.

In addition to volatility, it is also possible to express the relationship between two price movements directly as a number. The most important key figures here are the correlation and the beta factor.

Correlation

The correlation measures the relationship between two price movements and expresses this as a value between 1 and -1.

If a security and the DAX have a correlation of 0.8, this can be interpreted as meaning that this security will follow a price change in the DAX by the same percentage in 80% of all cases.

Beta factor

The beta factor can be calculated as a further key figure from the volatility and the correlation. It indicates whether a security has performed better or worse than another - usually an index. A beta factor of 1 means that both securities have developed in the same way. A beta factor higher than 1 indicates that the security has outperformed the index, while a lower beta factor indicates that the share's performance was below average.

Calculation formula

Beta factor(share,index) = Correlation(share,index) * (Volatility(share) / Volatility(index))

Negative beta factors are also possible if the price movements of the two securities move in opposite directions, for example in the case of puts.