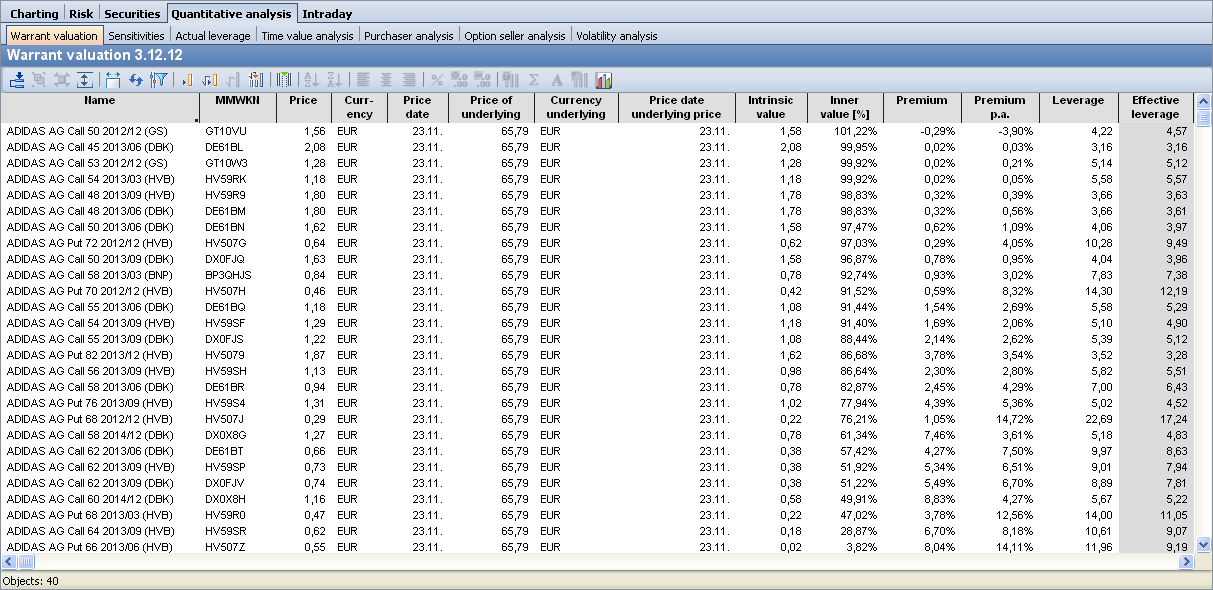

The "Warrant valuation" table contains all the standard key figures for options and warrants.

You can start the warrant valuation in the workspace of an underlying (for all warrants denominated in this underlying) or in the workspace of a folder or filter.

The details of the individual columns:

|

Column |

Description |

|---|---|

|

Name |

The name of the option or warrant. |

|

MMWKN |

The MMWKN of the option or warrant. |

|

Course |

The course on the specified date. |

|

Currency |

The price of the warrant or option is quoted in this currency. |

|

Course date |

The date of the price fixing. |

|

Underlying price |

The price of the underlying. |

|

Currency Underlying |

The currency in which the underlying is quoted. |

|

Price date Underlying |

The date of the base rate determination. |

|

Intrinsic value |

The intrinsic value of the bill is the difference between the base price and the strike price. It indicates the amount that can be realized by exercising the option or warrant. |

|

Inner value [%] |

Percentage of the intrinsic value of the warrant or option. |

|

Premium |

The premium of the warrant or option. Percentage by which the purchase of the underlying via the warrant is more expensive than the direct purchase via the stock exchange. The reverse is also true for put options. |

|

Premium p. a. |

The premium is converted to one year in each case. This enables a better comparison of warrants with different maturities. |

|

Lever |

The leverage indicates how the warrant would behave in purely mathematical terms in the event of a change in the price of the underlying asset. However, this value is not very meaningful. |

|

Effective leverage |

The effective lever is a further development of the lever described above. The premium is also included here. |

|

Fair price |

The fair price according to the Black-Scholes model is displayed here. |

|

Overvaluation |

This is the percentage over- or undervaluation of the actual price compared to the fair price. |

|

Break-Even |

The break-even indicates the minimum or maximum price that the underlying asset must reach on the warrant's maturity date in order for the buyer of the warrant to make a profit by exercising it. |

|

Basis volatility |

The volatility of the underlying asset over the specified period. |

|

Implied volatility |

The volatility that the warrant actually assigns to a security. Assuming that the actual price is identical to the fair price, it is possible to calculate the volatility that should be applied to this price. This is referred to as implied volatility. |

|

Combined volatility |

The combined volatility is calculated as the weighted average of the base volatility and the implied volatility. |

|

Last turnover |

Number of shares traded on the last trading day. |

|

Runtime |

Exact term of the warrant. |

|

Base price |

The price agreed when concluding an option transaction at which the buyer can sell or buy the underlying asset again up to the option date (or on the exercise date) (also: Strike). |

|

Bills: Shares |

Subscription ratio of the warrant. |

|

Annual high |

Highest price of the warrant since the beginning of the year. |

|

Low for the year |

Lowest price of the warrant since the beginning of the year. |

|

Security no. |

The security number of the option or warrant. |

|

WKN |

The securities identification number of the option or warrant. |