Situation before Infront Portfolio Manager Version 5.0

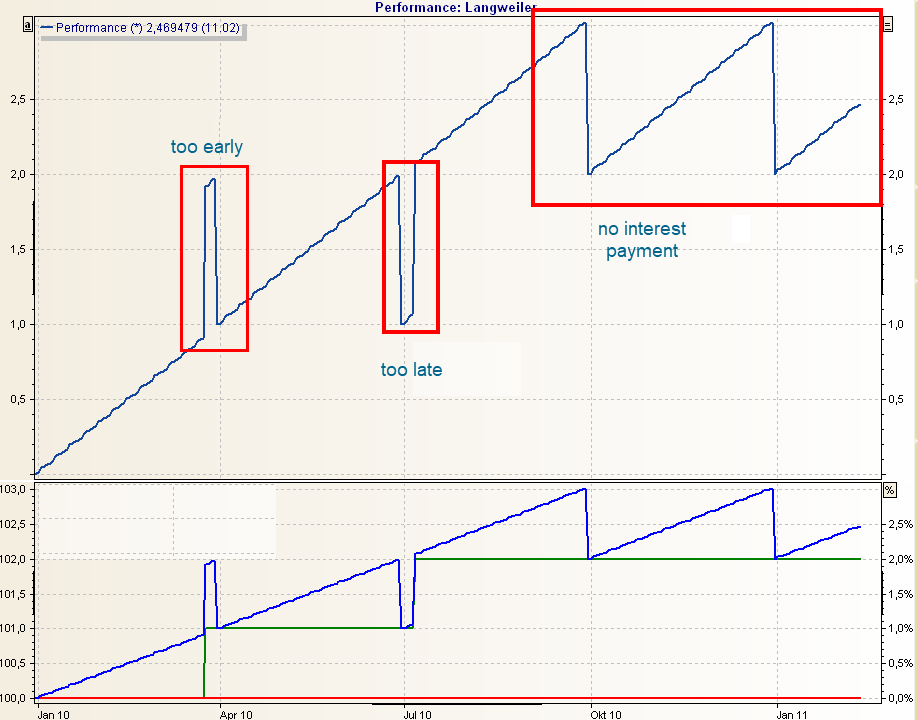

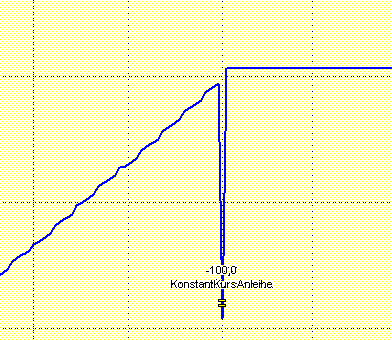

Accrued interest is calculated based on the master data (interest day method, interest interval, payment date) of the bond or account. This means that actual interest payments do not play a role in the calculation and must be posted in line with the master data in order to obtain a steady asset curve. If interest is booked at the wrong time, there will be jumps in performance and assets:

The illustration shows the performance of an overnight deposit with "inappropriate" interest payments. A method that takes into account interest payments and avoids such "jags" is desirable.

Basic idea

The accrued interest since the regular interest date of the last interest payment should be shown as the accrued interest of a position.

So if no interest is paid for an entire interest period, the accrued interest should simply continue to accrue until the time when interest is actually paid.

The following assumptions apply:

-

Interest is not paid much earlier than it is due.

-

Interest payments on an account are also part of the account.

-

If an interest payment is made late, the accrued interest is reset on the actual payment date to the value it would have had if payment had been made on time.

Differences between accounts and bonds

In the case of accounts, all interest accrued to date is shown as accrued interest, taking into account changes in the balance. Bonds have as accrued interest the amount of interest that has accrued between the last interest payment date and the current date with regard to the current portfolio.

The above assumptions for accountsmean that accrued interest is reset on the first interest payment after a regular interest payment date. The accrued interest is then the amount of interest that has accrued since the last interest payment date (to which the payment is attributed).

In the case of bonds , interest is calculated on the current portfolio on an interest payment date. If no interest payment is received, this defaulted interest is added to the accrued interest until an interest payment is received (then it is reset). If several interest payments are not made, the interest from several dates is included. In the case of inflation-linked bonds, the index ratio of the respective interest date is calculated - if several dates are missed, the appropriate ratio is calculated for each missed date.

Accounts: Behavior as of Infront Portfolio Manager Version 5.0

Accrued interest accrues until an interest payment is made. At this point, they are reset to the interest accrued between the last interest payment date and the current date. In contrast to bonds, the value date and not the booking date is decisive here. So if an interest payment is posted too early (before the actual interest payment date), but the corresponding value date is after the interest payment date, everything is fine, i.e. the assumption that interest is not paid too early is not violated.

Example of an interest-bearing account with missing and late interest payments.

Behavior before:

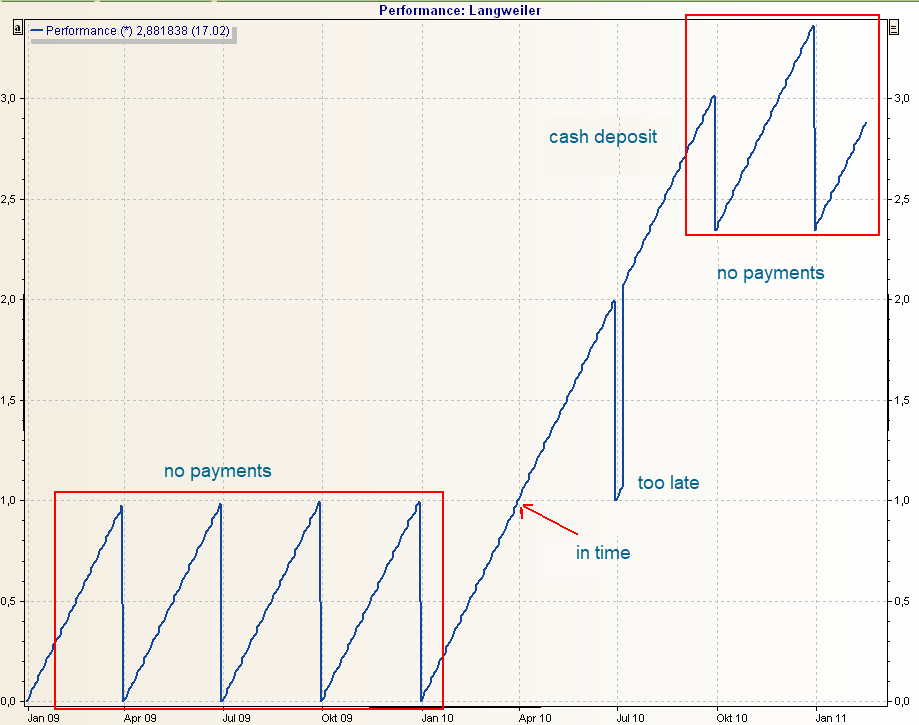

Behavior afterwards (same booking constellation):

Bonds: Behavior as of Infront Portfolio Manager Version 5.0

In the case of late payments, the interest on the bond behaves in principle like the interest on the account. If a bond position is closed out, the accrued interest (including the delayed interest) is also reset to 0.

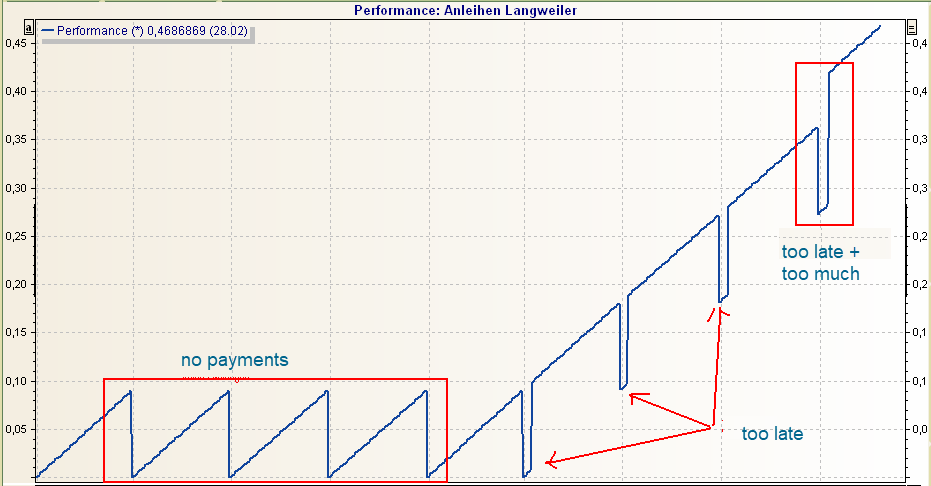

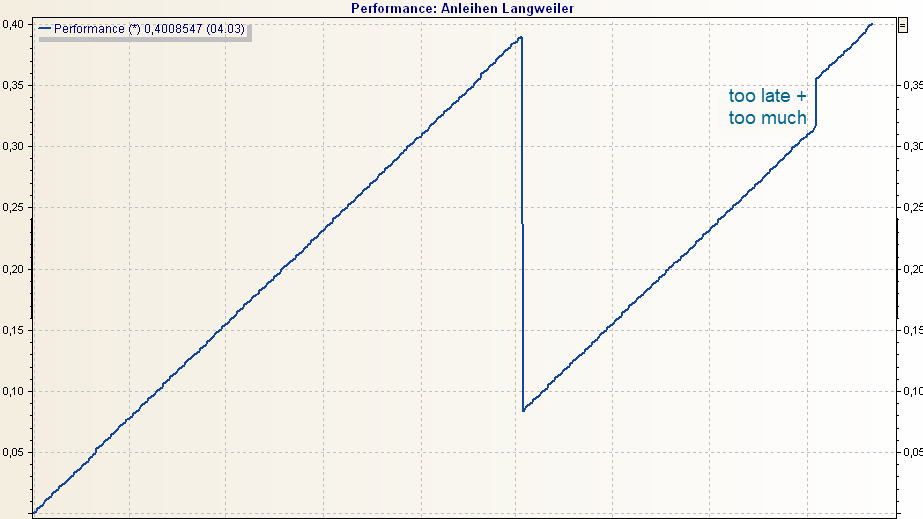

Bond with missing, late and excessive payments.

Behavior before:

The same booking history in Infront Portfolio Manager version 5.0 shows a behavior similar to the account:

Caution in the case of changes to holdings in the event of interest arrears (bonds):

If there are portfolio changes between the time when interest is expected and the time when it is paid, it is somewhat more difficult to check whether an interest payment is the correct amount.

Example of correct booking with purchase between nominal interest date and interest payment date:

Balance at the nominal interest date: 100, amount of the expected interest payment: 1.

Balance at the interest payment date: 200, interest payment: 1.

If you look at a statement of assets on the interest payment date, you might come up with the idea that the correct amount of the interest payment should be 2, since the balance is 200 and the accrued interest for a balance of 200 is exactly 2. It is therefore important to look at the nominal interest date.

If a position is closed for which there is still a accrued interest carryforward, this is reset to 0. Late payments are therefore only offset against existing items.

If accrued interest is still outstanding, closing out has the effect of reducing performance by the corresponding amount.

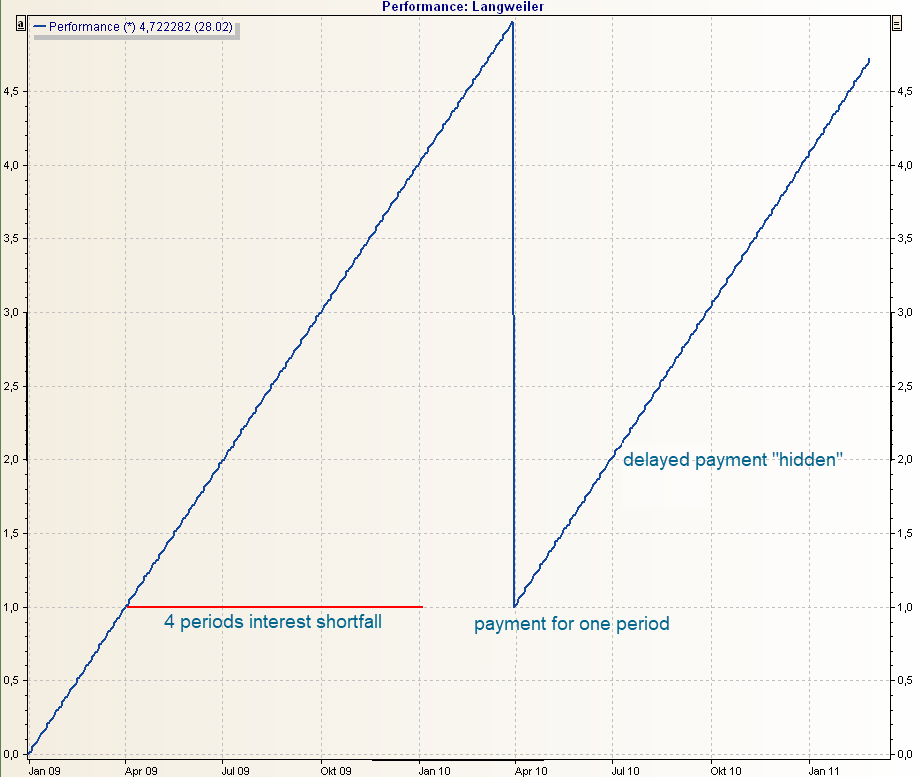

Side effect: Overlong coupons are possible

If an interest payment is suspended and made up for on the next date, this can simply be posted without any further action. In the example above, the interest for five periods would be paid on the first interest payment date instead of the interest for one period and everything fits together.

Other special cases such as the suspension of a date and catching up on repayment or complete failure of a payment must of course be mapped differently.

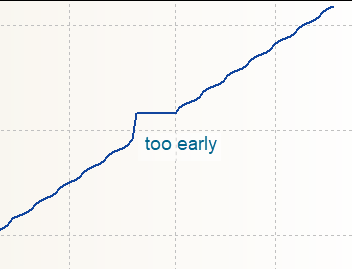

Coupons paid too early

Payments made up to 8 trading days before the actual interest payment date are added to the upcoming date. Accrued interest is set to 0 on the payment date. This looks like a staircase in the performance chart. The payment is too large, as it is for several days in advance, and the performance does not change until the interest payment date. It follows from this: The trend is initially steeply upwards and then horizontal until the interest payment date. Then back up again linearly.

Coupons that are more than 8 days before the interest payment date continue to generate jumps, as the period receives an "additional interest payment".

What is not possible:

-

Interest paid far too early

An interest payment may not be made more than 8 working days before the actual interest payment date. Interest payments that occur earlier are allocated to the preceding interest payment date if they do not themselves occur on an interest payment date. -

Interest payments in several tranches at different times

If part of the interest is paid today and another part tomorrow, the performance will collapse today (because too little interest was paid) and recover tomorrow (because interest was paid unexpectedly). -

Interest on closed bond positions

A bond position is closed out one day after the interest payment date and the delayed interest payment is made on the following day. Effect: On the day of sale, the securities account value is reduced by the accrued interest on the interest payment date (the delayed accrued interest is reset due to closing). On the following day, the value of the securities account jumps up again by the same amount, as an income payment is now made. The same applies to portfolio performance.

In the performance distribution, the performance of the item is shown without the delayed interest, as the balance is 0 at the time of payment (as division by 0 is not possible). However, the interest is listed as income (it does not have to be divided by 0).

Conclusion

You cannot book without any restrictions - there are certain assumptions on which the program is based. But the restrictions have been reduced compared to the old version.