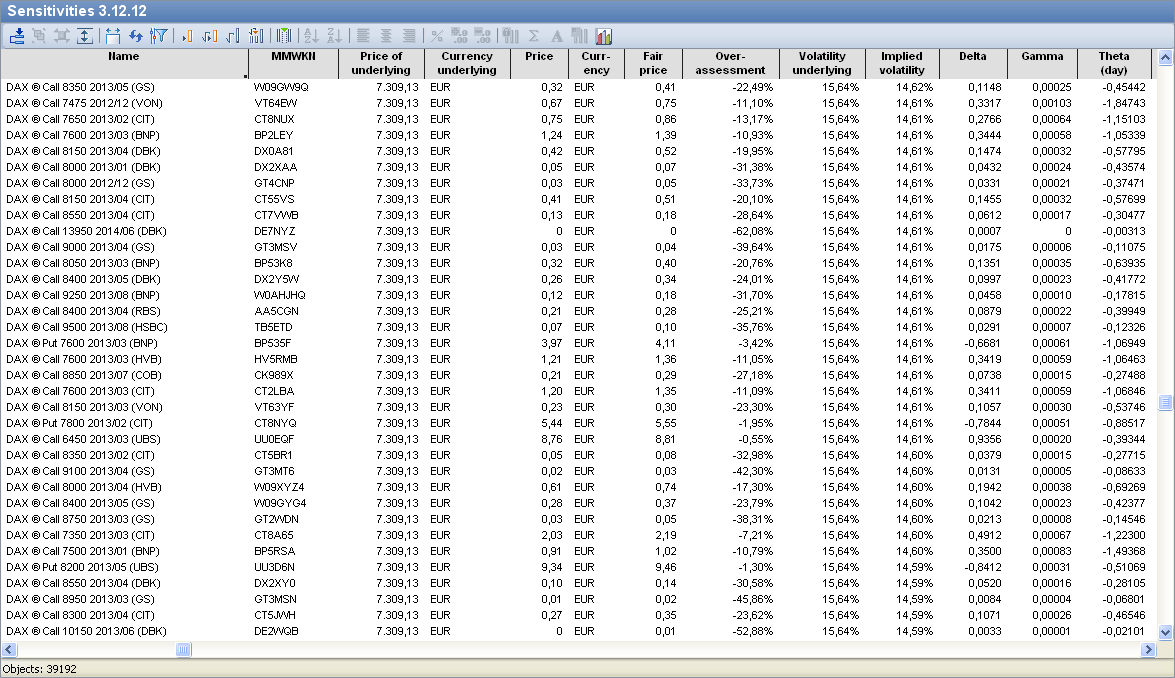

In addition to the pure listing of quantitative key figures, vwd portfolio manager also offers you the option of using the "Sensitivities" evaluation to determine how the price of an option also changes according to the Black-Scholes model when the individual parameters change.

The details of the individual columns:

|

Column |

Description |

|---|---|

|

Name |

The name of the option or warrant. |

|

MMWKN |

The MMWKN of the option or warrant. |

|

Underlying price |

The price of the underlying. |

|

Currency Underlying |

The currency of the underlying. |

|

Course |

The price of the option or warrant on the specified date. |

|

Currency |

The currency in which the option or warrant is quoted. |

|

Fair price |

The fair price according to the Black-Scholes model. |

|

Overvaluation |

The percentage over- or undervaluation of the actual price compared to the fair price. |

|

Volatility Underlying |

The volatility of the underlying asset over the specified evaluation period. |

|

Implied volatility |

The volatility that the warrant assigns to a security. Assuming that the actual price is identical to the fair price, it is possible to calculate the volatility that should be applied to this price. This is referred to as implied volatility. |

|

Delta |

The delta shows the dependence of the option price on the strike price. If the base price rises by one euro, the option price should theoretically rise by the delta value. The delta is always between 0 and 1 for calls and between -1 and 0 for puts. For example, if an option had a delta of 0.5, the option would rise by EUR 5 if the price of the underlying rose by EUR 10. As the option usually costs only a fraction of the underlying asset, the percentage profit from the option is much higher. Options with a delta close to 1 react almost like shares. These are usually options that are heavily in-the-money and have lost some of their speculative character. "At-the-money" calls usually have a delta of 0.5, while calls that are strongly "out-of-the-money" have very small deltas. |

|

Gamma |

The gamma measures the sensitivity of the delta to changes in the base price. The gamma expresses the amount by which the delta has changed with a change in the base price. The gamma must always be positive. Formula: Delta old + gamma = delta new |

|

Theta (day) |

The theta of the option shows the amount by which the time value is reduced daily. Options lose their premium over time until they only correspond to their intrinsic value on the expiry date. The shorter the remaining term of the option, the higher the theta. |

|

Vega |

Vega (sometimes also referred to as Eta) shows the dependence of the fair price on volatility. For example, the higher the volatility of a share, the more the option is worth. If the volatility of a share increases, the option increases by the value known as Vega. |

|

Rho |

The Rho (sometimes also referred to as the "epsilon") shows how the value of an option behaves when interest rates change by one percent. Since the interest rate for safe investments is also included in the calculation of the fair price, it is also possible to calculate how the value of an option changes if the interest rate changes. However, the influence of changes in interest rates is rather small. |

|

Omega |

The omega of the option or warrant. The omega indicates the percentage change in the option value assuming an underlying change of one percent. Omega is therefore a key figure that estimates the future leverage of an option. Due to the lower price, the option reacts more strongly in percentage terms than the underlying asset. |

|

Runtime |

The exact term of the warrant. |

|

Base price |

The price agreed when concluding an option transaction at which the buyer of an option can sell or buy the security again up to the option date (also: Strike). |

|

Bills: Shares |

The subscription ratio of the warrant. |

|

Security no. |

The security number of the option or warrant. |

|

WKN |

The securities identification number of the option or warrant. |