|

Range |

Value |

|---|---|

|

Market expectation |

Decreasing volatility

|

|

Construction |

x Calls long with strike price E1

|

|

Profit potential |

Limited |

|

Risk of loss |

Limited on one side |

|

Time effect |

? |

|

Volatility effect |

Negative |

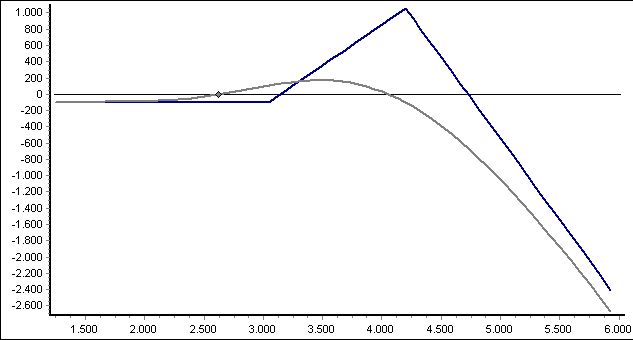

Market expectation

The market expectation for ratio spreads is decreasing price volatility. Ratio price spreads with calls also benefit from slightly rising prices.

Construction

Ratio price spreads consist of bought and sold options of the same option type.

To construct a ratio price spread with calls, you buy calls with a lower strike price and sell a larger number of calls with a higher strike price. Frequently used, sensible ratios of bought to sold options are: 2:3, 1:2, 2:5, 1:3. You can select these when choosing your strategy in the "Option Strategy Optimization" dialog box.

If the left "wing" of the curve is above the profit line, you will make a profit if the price of the underlying is below E1, as in this case you will have received more for the short calls than you invested for the long calls. This constellation is also known as a credit spread.

Profit potential

The profit potential is limited. The maximum profit is achieved if the price of the underlying asset is quoted at the higher strike price E2 at the end of the term. It is calculated as the difference between the base prices E2 and E1 less the premium expense.

Depending on the constellation, a profit or a loss is made on the left "wing".

Risk of loss

There is a one-sided limited risk of loss.

In addition to the possible limited loss on the left "wing", theoretically unlimited losses can occur on the right "wing" if prices rise sharply.

Time effect

The time effect depends on the price performance. It is positive in the expected range (near strike price E2), as the short calls are closer to the money there. It is negative on the left "wing". The effect of the time value naturally depends on the selected ratio.

Volatility effect

The volatility effect is negative on balance due to the higher number of short positions. This effect increases as the number of short positions rises.