|

Range |

Value |

|---|---|

|

Market expectation |

Rising volatility

|

|

Construction |

x Calls short with strike price E1

|

|

Profit potential |

Unlimited |

|

Risk of loss |

Limited |

|

Time effect |

? |

|

Volatility effect |

Positive |

Market expectation

Construct a ratio back spread if you expect an increase in volatility. With ratio back spreads with calls, you also speculate on rising prices.

Construction

Like any spread, the ratio back spread consists of bought and sold options of the same type. In the case of ratio back spreads with calls, you buy the calls with the higher strike price, which are cheaper.

However, since more calls are always bought than sold, i.e. the ratio spread is always in the form 1:2, 1:3, 2:3, 2:5 ..., you either pay a (net) premium when you open the position or you receive one.

Profit potential

The profit potential is unlimited if prices rise. The gains on the long calls more than offset the losses on the short calls.

The profit or loss potential is limited if prices fall. Depending on the constellation, you will receive a profit in the amount of the net premium or suffer a loss in this amount.

Risk of loss

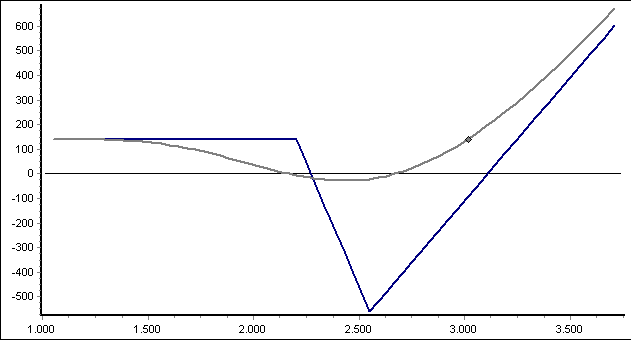

The risk of loss from a ratio back spread is limited. The maximum loss arises if the price of the underlying is quoted at the level of the strike price E2 on the maturity date.

Time effect

The fair value effect depends on the share price performance. If the price of the underlying is at the low strike price E1, the effect is positive; if it is close to E2, the effect is negative.

Volatility effect

The volatility effect is positive on balance, as more long than short positions are included. With increasing volatility, both the value of the options and the chances of greater price increases rise. This positive volatility effect is of course dependent on the number of long or short calls.