|

Range |

Value |

|---|---|

|

Market expectation |

Undirected strong price change

|

|

Construction |

Call long

|

|

Profit potential |

Unlimited |

|

Risk of loss |

Limited |

|

Time effect |

Negative |

|

Volatility effect |

Positive |

Market expectation

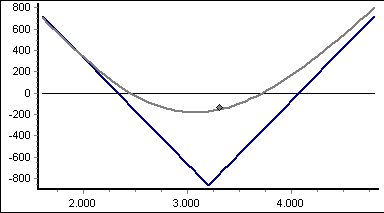

If you are assuming that prices will break out upwards or downwards and that volatility will rise as a result, a long straddle is a good option.

Construction

A long straddle consists of a call long and a put long with the same strike price and term. One of the two options therefore expires at the end of the term.

Profit potential

The profit potential is unlimited with strongly changing prices. The further the price moves away from the strike price, the higher the profit.

The lower break-even point is the base price minus the sum of the premiums paid, the upper break-even point is the base price plus the sum of the premiums paid.

Risk of loss

The risk of loss of the long straddle is limited. The maximum loss arises if the price of the underlying is at the level of the strike price, contrary to expectations. It then corresponds to the sum of the premiums paid.

Time effect

The time value effect is negative, as both positions are purchased and therefore both have negative time effects.

Volatility effect

The volatility effect is positive, as there is speculation on strong price changes and both call longs and put longs react positively to rising volatility.