|

Range |

Value |

|---|---|

|

Market expectation |

Decreasing volatility

|

|

Construction |

Call long with strike price E1

|

|

Profit potential |

Limited |

|

Risk of loss |

Limited |

|

Time effect |

? |

|

Volatility effect |

Neutral |

Market expectation

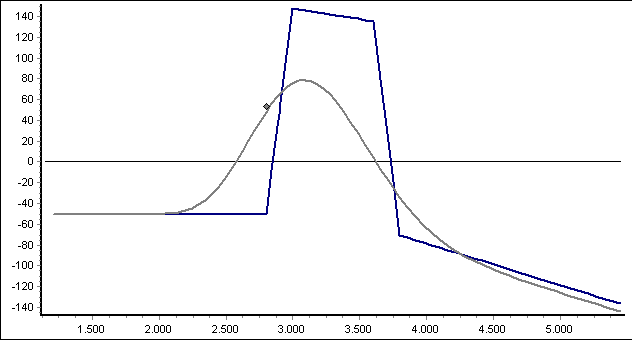

The long condor is a good choice if you expect little change in prices and therefore also lower volatility. The lower the volatility, the lower the probability that the price of the underlying will rise above the two outer strike prices.

Construction

Calls with four different strike prices are required to construct a long butterfly with calls. You sell the two calls at the middle strike prices and buy the two calls at the outer strike prices.

Alternatively, the long butterfly could also be interpreted as the simultaneous conclusion of a bull price spread (call long with E1 and call short with E2) and a bear price spread (call short with E2 and call long with E3).

A long condor can also be built up with puts, which leads to a similar profit and loss curve and therefore does not need to be described separately.

If you choose the same distance between the base prices, the result is a symmetrical curve; if the average base prices are far apart, the achievable profit is lower.

Profit potential

The profit potential is limited. The maximum profit is achieved if the price of the underlying asset is quoted between the average strike prices E2 and E3 at the end of the term. It is calculated as the difference between the base prices E2 and E1 less the premium expense.

The lower break-even point is the sum of the lower base price plus the premium expense, the upper break-even point at the upper base price minus the premium expense.

When considering the profit potential, you should also bear in mind the high transaction costs, which have a decisive influence in practice, especially with small contract volumes.

Risk of loss

The risk of loss of the long condor is limited. The maximum loss arises if the price of the underlying is either above the highest strike price or below the lowest strike price at maturity. It corresponds to the (net) premium paid for the position.

Time effect

If the price of the underlying does not change, there is a positive time value effect. The calls short are then roughly "at-the-money" with a high time value loss, the other two are far "in-the-money" or far "out-of-the-money".

The time effect becomes slightly negative if the price is below E1 or above E3, as a call long is then "at-the-money".

Volatility effect

The volatility effect is neutral.

Since two bought and two sold options form the long butterfly, changes in volatility do not have a significant effect on the position. A decrease in volatility is nevertheless advantageous, as the probability of unfavorable prices decreases.