Module "Advanced Technical Analysis"

Once the trading system and the input list have been defined, you can carry out the first optimization.

-

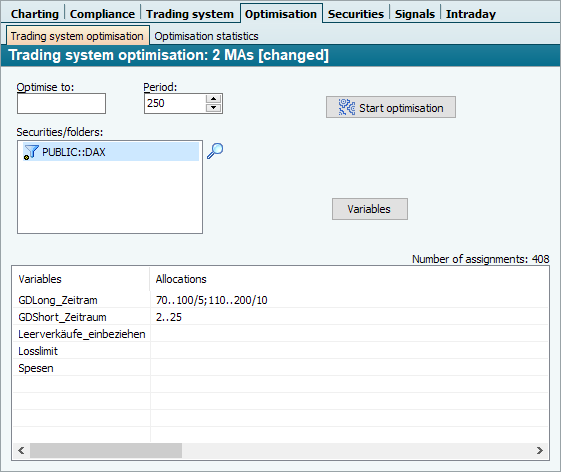

Open the workspace of the trading system and switch to the "Optimization" tab and then to "Trading system optimization".

-

If you leave the "Optimization to" field empty, the current date will be used (default).

-

The "Period" field specifies the period over which the optimization is to be carried out; depending on the trading system, between 120 and 500 trading days (i.e. around 4 to 24 months) are possible.

-

The papers to be optimized are entered in the "Securities/folder" field. Drag and drop the input of the trading system into this field.

You can also drag other Explorer objects such as securities accounts, individual securities or folders into the input field. -

The lower input table is used to assign values to the variables to be optimized. The values specified here are then optimized. No optimization is carried out for values where the "Assignments" column remains empty - the default value from the definition dialog is used.

-

You can define not only the assignments, but also the step sizes for the optimization. 0..30/5 means, for example, that the values 0,5,10,15 etc. are tested up to 30, i.e. in steps of 5.

Further details can be found in the section Optimize trading systems. -

Start the optimization by clicking on the "Start optimization" button.

You can display statistics of the optimized values on the "Optimization statistics" tab.