Module "Portfolio Service Extended Portfolio Analysis"

You can find the "Performance contribution" evaluation in the workspace of portfolios, owners or groups on the "Performance" worksheet, for example.

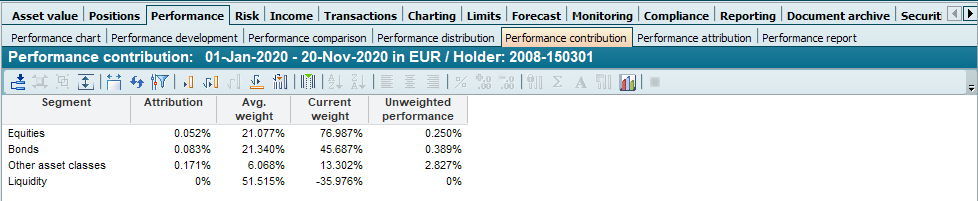

Segmentation by asset classification was selected in the chart. The following information is calculated for the individual segments and shown in the table:

|

Column |

Description |

|---|---|

|

Segment |

The name of the segment. |

|

Attribution |

The performance contribution of the segment in the set period with the actual weighting of the segment over the period (<weight average>). The weighting refers to the total assets including liquidity (account balances) of the holder under review. If you do not want to take the account balances into account when determining the performance contributions, deactivate the "Take account balances into account" parameter. |

|

Average weight |

Average weight of the segment during the period. It is necessary to specify an average weighting, as the composition of the portfolio may change during the period under review due to reallocations. The average weight is calculated as the sum over all periods of (weight of the segment at the start of the period * period length in days) / total length in days. The number of days is calculated depending on the setting of the "Calculate average available capital on trading days (otherwise calendar days)" checkbox on the "Securities account" tab in the general settings. |

|

Current weight |

Weight of the segment on the evaluation date. This information is purely informative and is used for comparison with the value in the "Average weight" column. |

|

Unweighted performance |

The (time-weighted) performance of the segment in the set period with a theoretical weighting of 100% (performance that would have been achieved if 100% had been invested in this segment). The unweighted performance of a segment does not necessarily have to be calculated over the entire evaluation interval, but takes into account exactly the days on which the input object (portfolio, holder...) was invested in this segment. |

The calculation of the "Attribution" column is based on the securities positions underlying the segment. The securities performance, in turn, is calculated as a time-weighted performance taking into account income and capital measures. If there are no changes in the securities positions underlying a segment during the period under review, e.g. through purchases, sales or income postings, the performance contribution of the segment is simply calculated as the weighted sum of the performance values of the individual securities positions.

As a rule, however, there are always reallocations during the period under review. Determining segment performance then becomes more complicated. In line with the calculation of portfolio performance using the time-weighted method (see section Calculation of performance), the period under review is divided into several periods so that no change in weighting due to purchases, sales, etc. has taken place within the individual periods (a change in weighting due to price changes naturally takes place in every period). The initial weight and performance are now determined for each period and each security position. The segment performance values within the individual periods can be calculated as the weighted sum of the performance values of the individual securities positions in the same period. The segment performance over the entire period under review is then calculated by geometrically linking the segment performance values of the individual periods.

|

Segments |

Positions |

Period 1 |

Period 2 |

Period 3 |

Total |

|---|---|---|---|---|---|

|

S1

|

Share A |

gA,1 / pA,1 |

gA,2 / pA,2 |

gA,3 / pA,3 |

|

|

Share B |

gB,1 / pB,1 |

gB,2 / pB,2 |

gB,3 / pB,3 |

||

|

Share C |

gC,1 / pC,1 |

gC,2 / pC,2 |

gC,3 / pC,3 |

||

|

Total S1 |

S1(P1) |

S1(P2) |

S1(P3) |

S1 |

|

|

S2

|

Share D |

gD,1 / pD,1 |

gD,2 / pD,2 |

gD,3 / pD,3 |

|

|

Share E |

gE,1 / pE,1 |

gE,2 / pE,2 |

gE,3 / pE,3 |

|

|

|

Total S2 |

S2(P1) |

S2(P2) |

S2(P3) |

S2 |

|

In the table

gA,1: Weight of share A at the beginning of period 1

pA,1: Performance of share A in period 1

With ri,j as gi,j*pi,j applies:

S1(P1) = rA,1 + rB,1 + rC,1 (performance contribution segment 1 in period 1)

S1(P2) = rA,2 + rB,2 + rC,2 (performance contribution segment 1 in period 2)

S1(P3) = rA,3 + rB,3 + rC,3 (performance contribution segment 1 in period 3)

S1 = (1+S1(P1)) * (1+S1(P2)) * (1+S1(P3)) - 1(geometric link)

S1 is the performance contribution for segment 1.

The same applies to the S2 segment.

Read about the general formulas: Fischer, Performance Analysis in Practice, Oldenbourg, ISBN 3-486-25628-9

It should be noted that the total performance in the example cannot simply be determined by S1+S2, but as a geometric combination of the sum of the individual segment performance contributions as follows:

P = (1+S1(P1)+S2(P1)) * (1+S1(P2)+S2(P2)) * (1+S1(P3)+S2(P3)) - 1

Therefore, no totals should be shown in the evaluations.