|

Range |

Value |

|---|---|

|

Market expectation |

Rising prices |

|

Construction |

Call long |

|

Profit potential |

Unlimited |

|

Risk of loss |

Limited |

|

Time effect |

Negative |

|

Volatility effect |

Positive |

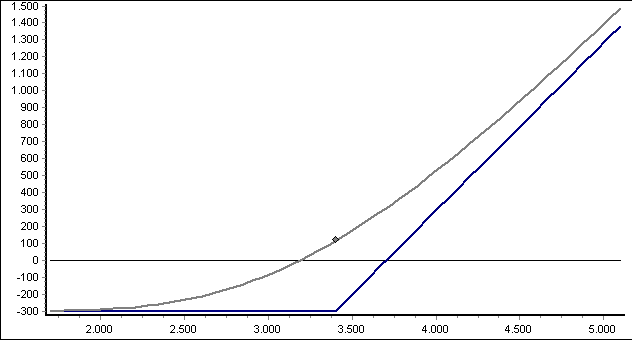

Market expectation

You should choose your calls depending on your market expectations. The more positive these expectations are, the further the calls may be "out-of-the-money" when purchased, i.e. the price may be (significantly) below the strike price.

If, on the other hand, you expect prices to rise only slightly, the calls should be "in-the-money" or at least "at-the-money".

Profit potential

The break-even point for the call long is the strike price plus premium (in the illustration the intersection with the horizontal line at profit 0).

If the price of the underlying asset rises significantly above the strike price, the value of the call increases more than the underlying asset due to the leverage effect.

Risk of loss

The maximum loss is limited to the option premium paid and occurs if the price of the underlying is below the strike price on the expiry date of the warrant.

If the price is between the strike price and break-even, you suffer a partial loss.

Time effect

The time effect is negative. Since the chances of price increases also decrease as the remaining term decreases, the time value of a call long decreases. On the maturity date, the fair value is 0.

Volatility effect

If the volatility of the underlying increases during the remaining term, the value of the call also increases.