|

Range |

Value |

|---|---|

|

Market expectation |

(Slightly) falling prices |

|

Construction |

Call short with strike price E1

|

|

Profit potential |

Limited |

|

Risk of loss |

Limited |

|

Time effect |

? |

|

Volatility effect |

Neutral |

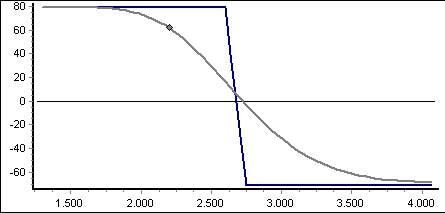

Market expectation

If you expect prices to fall slightly, it is advisable to construct a bear price spread. Select the strike price E1 in such a way that you do not consider it likely that the price will fall below this value.

Construction

Price spreads consist either only of puts or only of calls. A long and a short position are taken on the same type of option, i.e. the options differ only in the strike price, not in the term.

In addition to the bear price spread with calls as in the example above, there is also the bear price spread with puts. Here too, the put with the lower strike price is sold and the put with the higher strike price is bought. The result is the same profit profile.

Profit potential

Bear price spreads with calls initially bring a credit in the amount of the difference between the two premiums, as the call short always flows in with the higher premium (lower strike price) than the call long.

The break-even point for the bear price spread with calls is the lower strike price E1 plus the difference in option premiums.

The maximum profit corresponds to the difference between the option premiums. It is achieved if both calls expire, i.e. the price of the underlying is below E1 on the expiry date.

For bear price spreads with puts, on the other hand, you must first pay the difference between the two premiums, as the put with the higher strike price is more expensive.

The break-even point for the bear price spread with puts is the higher strike price E1 minus the (paid) difference in option premiums.

You will receive the maximum profit for bear price spreads with puts if the underlying is quoted lower than E1.

Risk of loss

The maximum loss of the bear price spread with calls is limited, because if the price rises above E2, both calls are exercised.

The maximum loss is the difference between the two base prices (E2 - E1) less the difference in premiums (received).

If the price of the underlying is between the two strike prices, this results in a positive or negative partial profit. Only the call with the lower strike price is exercised. If the resulting loss for you as the writer is higher than the premium received, a partial loss arises from the overall position, and a partial gain in the opposite case.

For bull price spreads with puts, the maximum loss is the difference (paid) between the original premiums.

Time effect

The time effect cannot be specified precisely, as it depends crucially on the price of the underlying asset. If the share price is negative (price below break-even), the time effect is positive; if the price is above break-even, the time effect is negative.

Volatility effect

The volatility effect of the overall position is neutral, although of course the two warrants react. However, since there is a long and a short position of the same maturity for each option type, the change in volatility has no effect.