Exposure analysis

Module "Portfolio Service Extended Portfolio Analysis"

The Infront Portfolio Manager provides you with three standard templates for exposure analysis:

- Exposure analysis (table)

- Report Exposure Analysis Futures

- Report Exposure analysis DTG

In the "Exposure analysis" tabular evaluation described here, you can use a parameter to switch between the analysis for futures and forward exchange transactions. Two separate reports are available here for customer reporting.

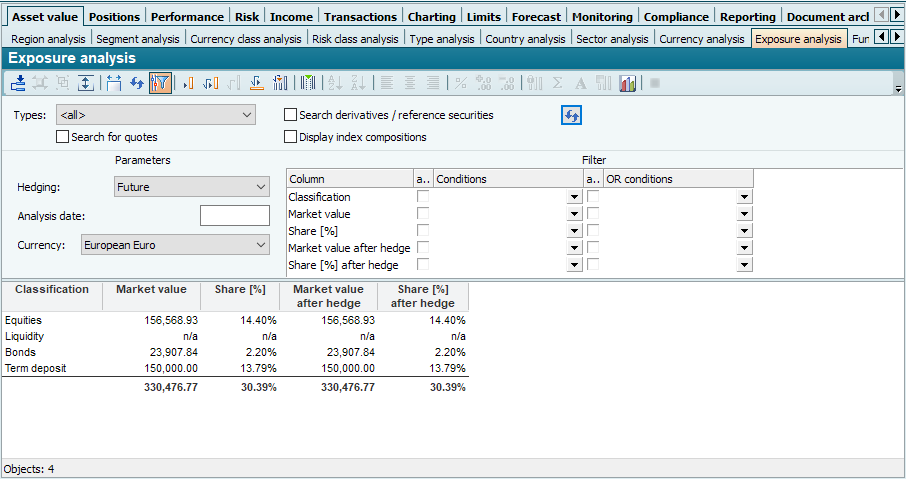

With the "Exposure analysis" evaluation, you can see at a glance the effects of your hedging strategies via futures or forward exchange transactions on the individual asset or currency classes.

You can find the "Exposure analysis" in the workspace of holders or portfolios on the "Assets" worksheet, for example.

You can see the following columns in the "Exposure analysis" table:

Column | Description |

|---|---|

Classification | In this column you can see the individual asset classes. Depending on the setting of the "Hedging" parameter, the individual currencies ("Forward exchange transaction" hedging) or the individual asset classes ("Future" hedging) are displayed here. |

Market value | The market value of the respective asset class before hedging in evaluation currency. |

Share [%] | The percentage share of the respective asset class in the overall portfolio in relation to the market value before hedging. |

Market value after hedge | The market value of the respective asset class after hedging in evaluation currency. |

Share [%] by hedge | The percentage share of the respective asset class in the overall portfolio after hedging. |

Hedging of asset classes:

If hedging is carried out with futures, a hedging class must be assigned to each future used in vwd portfolio manager. Use the new user-defined field "Hedging class" for this purpose.

The simplified formula for exposure is as follows: Contracts * contract value * market value.

The real exposure is then offset against the market value of the liquidity and the hedging class.

Long:

Liquidity - real exposure

Hedging class + real exposure

Short:

Liquidity + real exposure

Hedging class - real exposure

Hedging of currencies:

For the exposure to DTGs, the investment and the future inflow amount are considered. The MM-Talk function Purchase priceDev is used for the investment in evaluation currency. The amount is then deducted from the market value of the outflow currency. The future inflow amount in inflow currency can be called up with the MM-Talk function Balance and must be converted into the evaluation currency. This amount is then added to the market value of the inflow currency of the forward exchange transaction.

Siehe auch: